Key Takeaways

Global M&A activity gained substantial momentum throughout 2024. Asset quality was mixed across the market as a whole, driving strong competitive tension and premium valuations for top-quality businesses while impacting timelines and diligence requirements in some cases.

Impatience has been building in the market for high-quality opportunities, and investors are eager to deploy capital and generate liquidity. Harris Williams has seen a steady increase in activity as valuation gaps narrow, alternative solutions gain traction, and buyers and sellers continue to take thoughtful approaches to entering the market.

Against this backdrop, 2025 should see continued strengthening in the market. With a robust backlog of top-quality businesses, Harris Williams is excited to help a diverse range of investors and company leaders make the most of the M&A and private capital markets in 2025 and beyond.

2024: Momentum and Mixed Quality

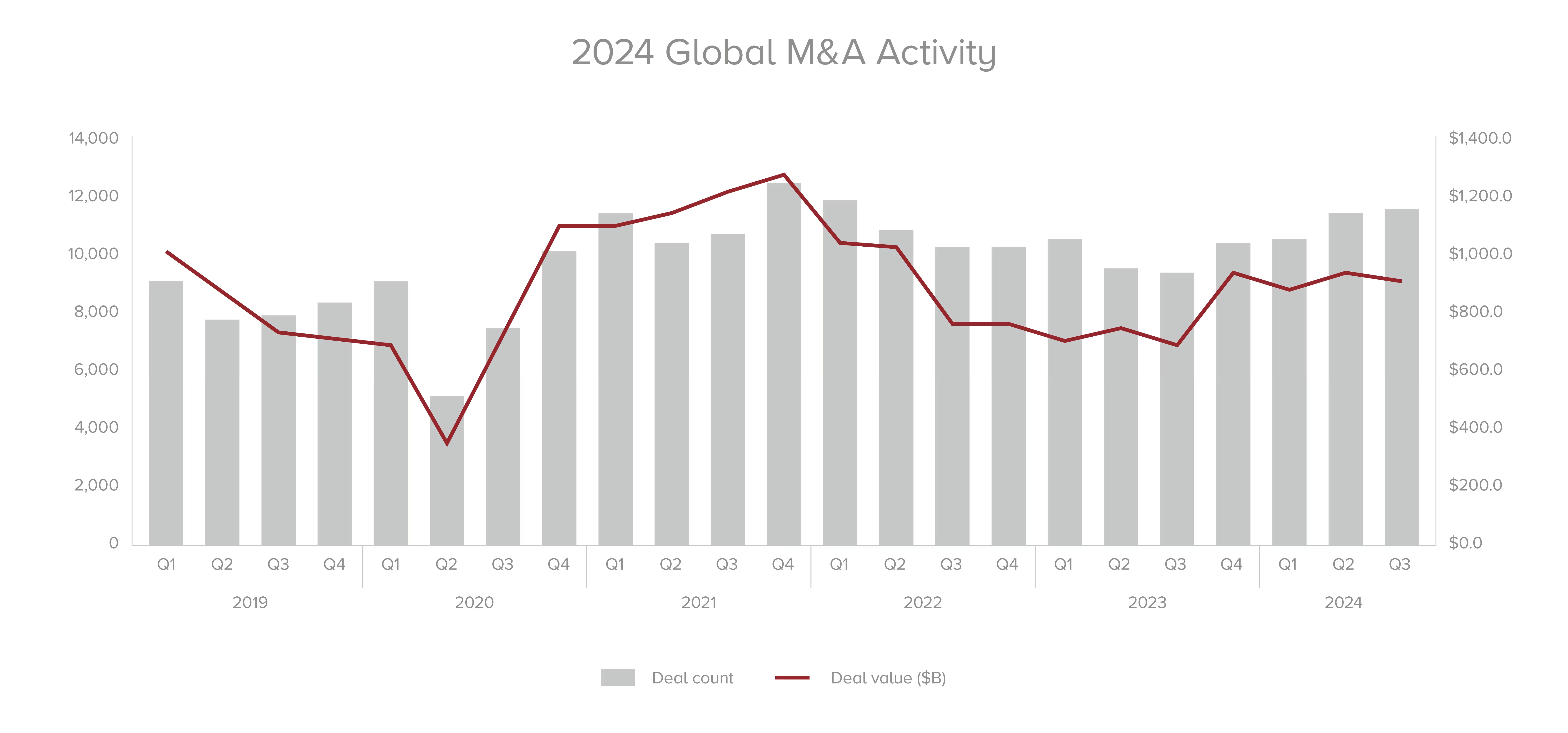

The global M&A market steadily gained momentum throughout 2024. In fact, as of the end of the third quarter, global M&A activity had increased by 27.6% in terms of value and 13.3% in volume year over year (Figure 1).ᶦ

Figure 1: 2024 Global M&A Activity

Source: Pitchbook

In the U.S., private-equity-backed platform LBOs were up 28.4% year over year by value and 14.3% by volume over the same period.ᶦᶦ "There were certainly more opportunities for engagement in 2024. While the market for sub-$500 million total enterprise value transactions was the most active, many of the industries and sectors Harris Williams specializes in saw an increase in larger transactions as well," notes Frank Mountcastle, a managing director and the head of M&A at Harris Williams. "Great examples include NSI Industries, CLEAResult Consulting, Communications & Power Industries Electron Device Business, RJW Logistics Group, GeoStabilization International, Mott Corporation, and several others."

As in the U.S., European M&A markets saw a gradual improvement in transaction volume throughout 2024. "Activity was strongest in terms of take-privates, add-ons, carve-outs, and secondaries, with many investors focusing on portfolio management and familiar businesses and sectors," says Bob Baltimore, co-chief executive officer.

Meanwhile, a diverse range of Asian buyers continued to seek opportunities to invest in Western markets and businesses in 2024. "The imperative to invest capital remains strong," says Daniel Wang, a managing director and head of Asia-Pacific and Sovereign Wealth Funds. "In addition to financial sponsors, we've seen Sovereign Wealth Funds from Asia and the Middle East continuing to be active, including partnering with Western private equity firms on larger transactions."

Although global M&A activity was solid in 2024, asset quality was mixed, with a relative lack of exemplary platform opportunities driving strong competitive tension and optimal valuations for the best of the best. This has sparked considerable interest in creative alternatives. "We're working with clients on an increasing variety of liquidity events, including continuation vehicles, structured recaps, and minority sales," says Andrew Gulotta, a managing director in the Harris Williams Private Capital Advisory Group. "These solutions can provide liquidity and growth capital, while giving sponsors more ways to participate in the long-term growth of great businesses and industry sectors."

"This increased optionality has changed the market permanently, and we expect our clients to continue to embrace more alternative strategies," adds Baltimore. "Our industry-focused bankers are seamlessly integrated with our private capital advisory team, combining their expertise to advise on a growing range of creative approaches suited to this dynamic environment."

2025: A Time for Action

Amid these dynamics, Harris Williams saw steadily growing transaction volumes in 2024, a trend we expect will continue in 2025. Indeed, the relative lack of urgency that shaped M&A in early 2024 has already shifted, and our backlog of top-quality companies entering 2025 is robust and continues to grow.

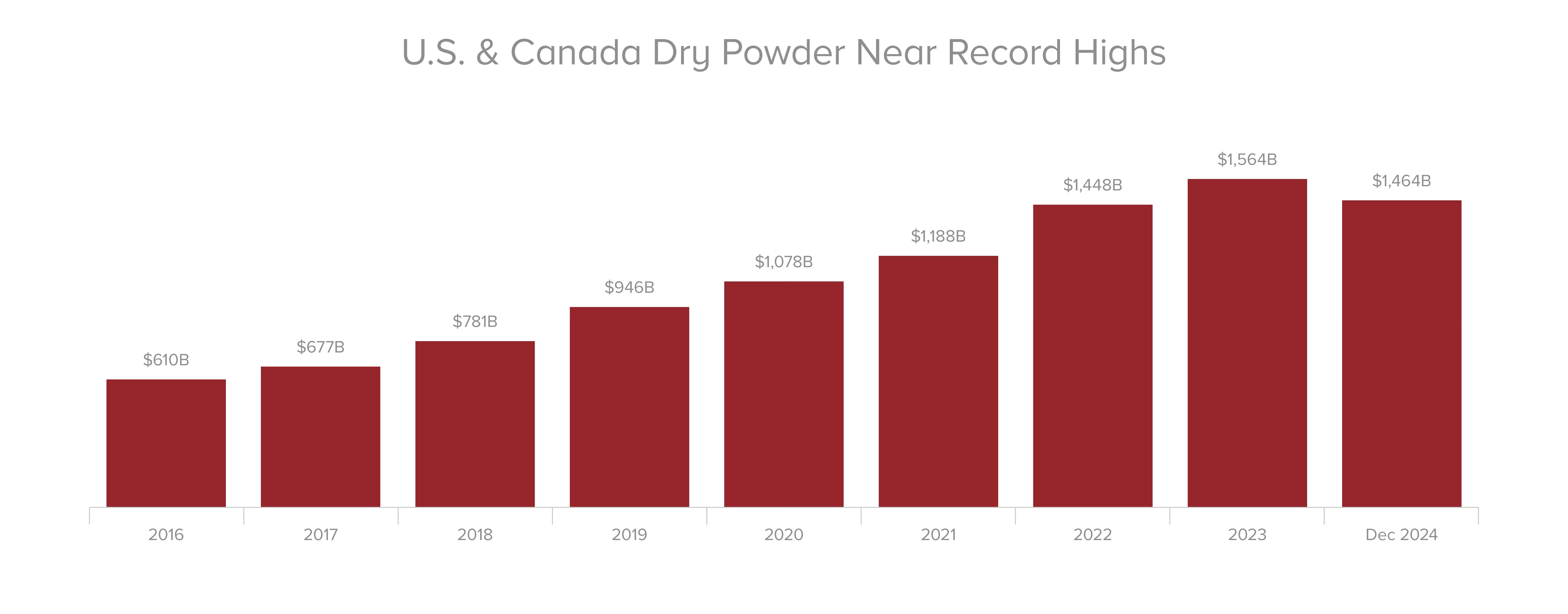

Several factors will contribute to this steady increase in activity in 2025. Private equity groups are looking to put capital to work, and the dry powder overhang remains large and is aging (Figure 2). In fact, a record 26% of dry powder was raised more than four years ago, and investors are increasingly eager to realize returns.ᶦᶦᶦ

Figure 2: U.S. & Canada Dry Powder Near Record Highs

Source: CapIQ

PEGs have also been hesitant to part with winning businesses amid some valuation gaps between buyers and sellers, leading to longer hold durations in some cases. These longer holding periods mean PEGs own nearly twice the number of companies they owned just a few years ago, stretching their resources and bolstering the imperative to transact sooner than later.ᶦᵛ This is further intensifying the drive to generate liquidity and balance deployment with fundraising.

"We're working with many clients focused on preparing for first-half 2025 launches," notes John Neuner, co-chief executive officer. "2024 was a year for private equity groups to focus on bolstering the quality of their existing portfolio companies, so we're optimistic that 2025 will see more large and desirable platforms entering the market."

"The combination of elongated hold periods, deal team capacity constraints resulting from decreased exit activity in the last two years, and persistent DPI pressure from LPs are all likely to drive increased deal volume over the next several quarters," adds Bruce Kelleher, a managing director and group head of the financial sponsor coverage team. "As sellers increasingly focus on generating liquidity, valuation gaps should moderate and become less of a governor to deal flow."

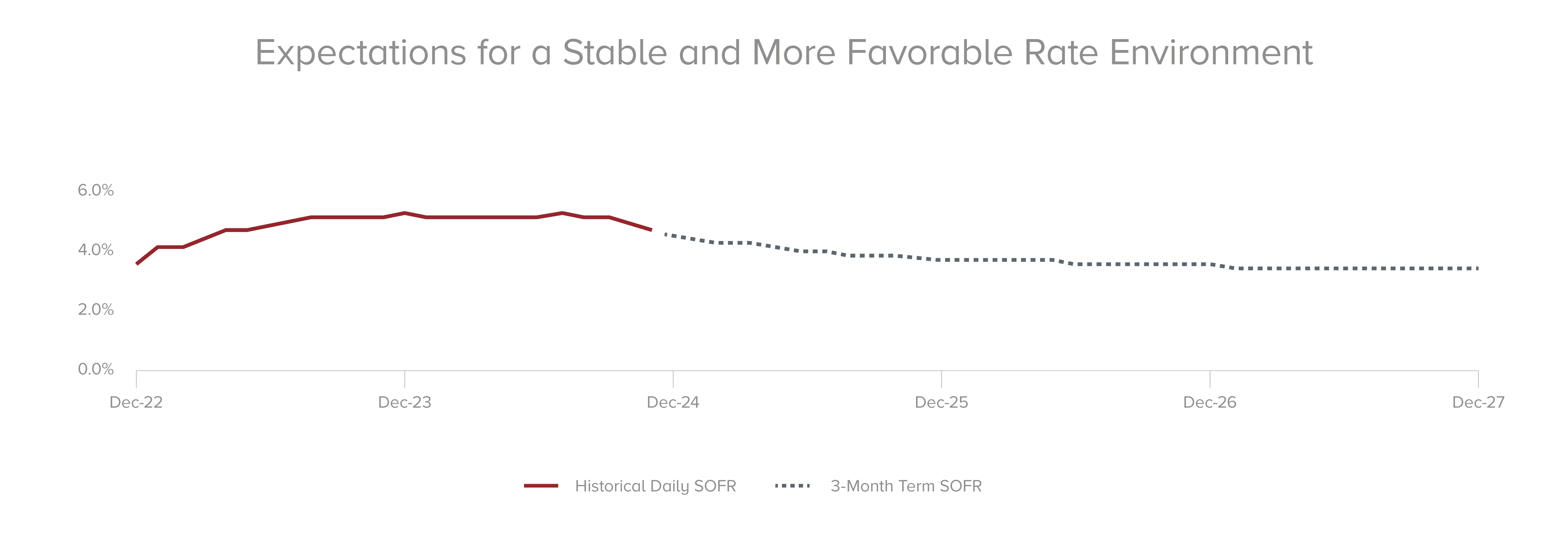

And, while the Fed's rate path going forward is uncertain, the consensus view is that rates will either stay flat or fall further in the months to come (Figure 3).

Figure 3: Expectations for a Stable and More Favorable Rate Environment

Sources: CapIQ, Pensford Financial

"While additional rate cuts would certainly produce an element of momentum, they are not necessary for M&A to rebound," notes Bill Watkins, a managing director. "Most investors have already priced in the cost of capital, and we have been in a higher rate environment now for a couple of years." Watkins adds that financing costs are easing in European markets as well, with rate cuts in 2024 from both the European Central Bank and the Bank of England.

In addition, with the evolution and creativity of private capital, buyers and sellers can transact at will and are not waiting for another rate cut. "Leverage has not been an issue for most Harris Williams clients this year," says Watkins. "With so much capital on the sidelines, the private credit and BSL markets are being more aggressive than at any time over the past two years. There is real optimism building that new deal flow—not just add-ons, dividend recaps, and re-pricings—will accelerate throughout the year."

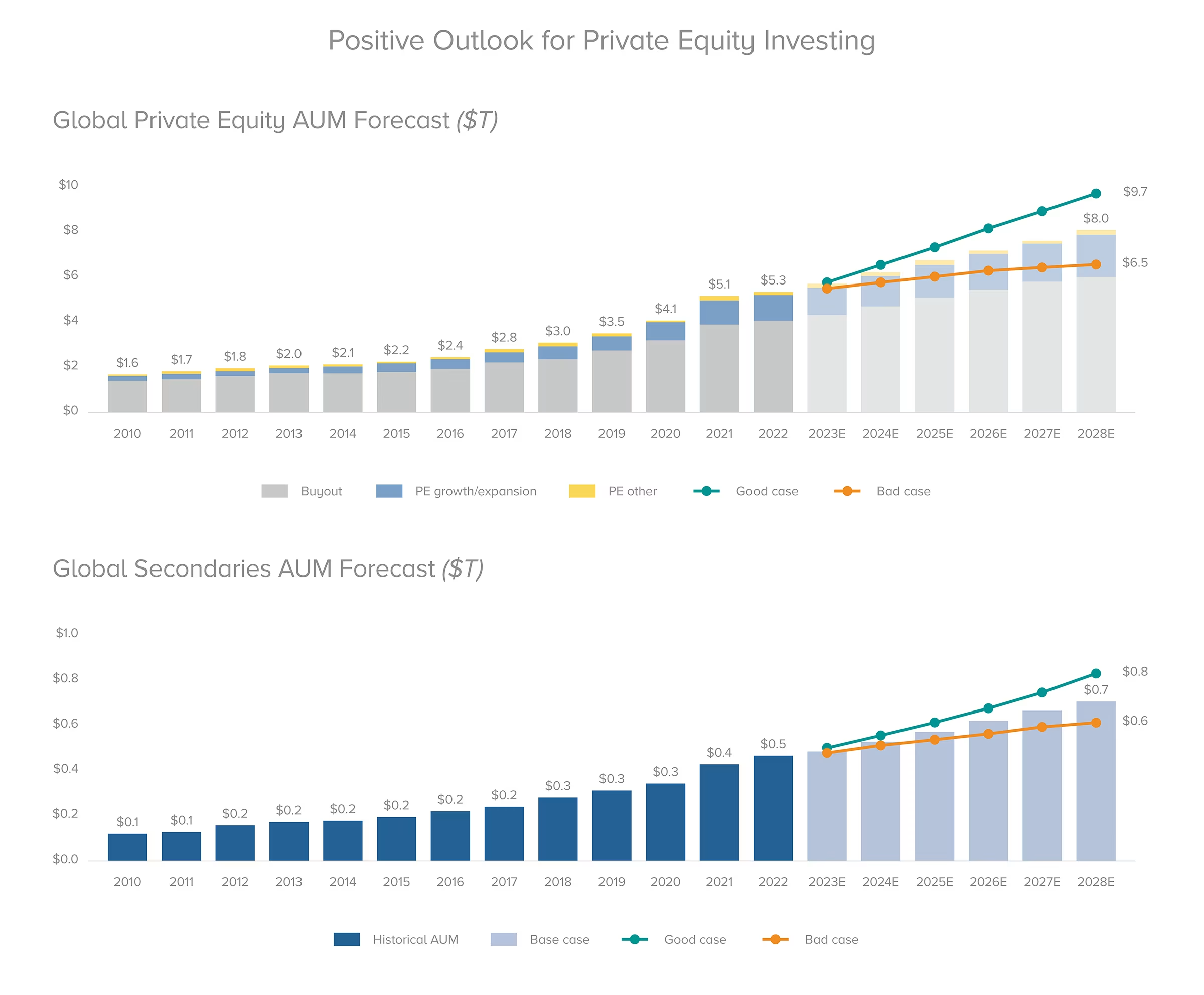

Indeed, the outlook for global private equity investing is very encouraging, with positive growth forecasts for assets under management and for secondaries (Figure 4).

Figure 4: Positive Outlook for Private Equity Investing

Source: Pitchbook

"The PE investing model continues to benefit from ongoing innovation and adoption," says Baltimore. "Looking ahead, there's immense opportunity for a growing range of investors to participate in the growth."

Making the Most of 2025

While risks remain—including evolving antitrust dynamics, potential new tariffs, and global geopolitical uncertainty—a variety of encouraging trends are driving more confidence among buyers and sellers.

"With the U.S. presidential election behind us, consumer spending and financial health remaining robust, the rate environment stabilizing, and company performance trending upward, we think 2025 will be a good year for continued strengthening in the M&A market," says Neuner.

With M&A activity poised to steadily build throughout 2025, several key practices can help buyers and sellers make the most of the opportunity.

Embrace optionality

The realities of 2024—longer deal durations, valuation gaps, and macroeconomic challenges—have sparked considerable innovation while giving buyers and sellers more options to consider. Going forward, both groups should consider all available options to achieve their specific goals.

"Our long-term strategy is to support our clients through a growing variety of challenges and opportunities, whether their goal is to deploy capital as conditions improve, exit a great company at optimal value, retain a stake in a high-performing business, or generate liquidity for growth or for investors," says Baltimore.

"One of the key success factors for Harris Williams is tailoring our approach to specific client circumstances," adds Neuner. "As we enter 2025, the environment remains complex and dynamic. It's essential to deeply understand our clients' objectives and develop strategies to unlock the full value of their businesses. Early and upfront work and direct dialogue with buyers and sellers remain critical."

Focus on the company's unique success story

While many signs point to a steady recovery in 2025, the market still has the potential for new disruptions. As such, potential buyers will remain focused on proof points showing the long-term viability of the company's strategy.

"Investors are looking for evidence of progress toward key initiatives, and they want to be assured that recent performance accurately reflects longer-term growth potential," says Mountcastle. "Our role as trusted advisors is to fully understand the nuances of our clients' businesses and help them bring their data-driven growth story to the market. There's both a qualitative and a quantitative element to those stories, and they must include all the details potential buyers will want."

Budget time to transact

Despite our anticipated growth in transaction volume, the bar for diligence will remain high among buyers. With a degree of complexity set to remain intact in 2025, buyers and sellers must set aside enough time and resources to successfully execute their chosen strategies. Additional time will likely be required for earlier and more in-depth diligence and analysis, consideration of emerging factors such as tariffs and China exposure, and the additional work required to satisfy new HSR requirements.

"To avoid deal delays, companies should be systematic about maintaining the data and documents the government wants to see," says Mountcastle. "At the same time, competition for the strongest opportunities will continue to be intense as investors feel the pressure to put money to work. It's key to hit the ground running with a seasoned team, including antitrust counsel and advisors well versed in specific industry and market dynamics."

A Strong and Steady Rebound

While M&A in 2024 was influenced by a somewhat tentative mindset among many buyers and sellers, 2025 is shaping up to be a year of action, with the easing of liquidity constraints, valuation gaps, and macro uncertainty.

"As investors continue to successfully exit portfolio companies, they will free up capacity to invest in new opportunities and put their substantial dry powder to work," says Neuner. "And, as potential sellers see more transactions occurring in their respective industries, many will gain the confidence and conviction to get off the sidelines. Likewise, as LPs continue to see increased liquidity and returns, fundraising headwinds are poised to ease."

"Many of our clients are eager to launch, and we're continuing to see strong deal and pitch activity, combined with a healthy backlog," says Baltimore. "With ongoing macroeconomic strength and a more stable environment, conditions are favorable for a strong and steady rebound throughout 2025."

With a healthy slate of transactions and significant growth in the forecast, we are thankful for the trust our clients place in us and the opportunity to help them unlock the value in their businesses in 2025 and beyond.