Article - February 6, 2020

Employer Health: Third-Party Administrators

Healthcare costs are employers` biggest non-payroll expenses, and they continue to climb. In response, a host of innovative employer health businesses have emerged to help employers better manage those costs and improve employee wellness and satisfaction.

In this article series, Harris Williams senior professionals from our Healthcare & Life Sciences (HCLS) Group, Business Services Group and Technology Group explore the key subsectors of the growing employer health industry.

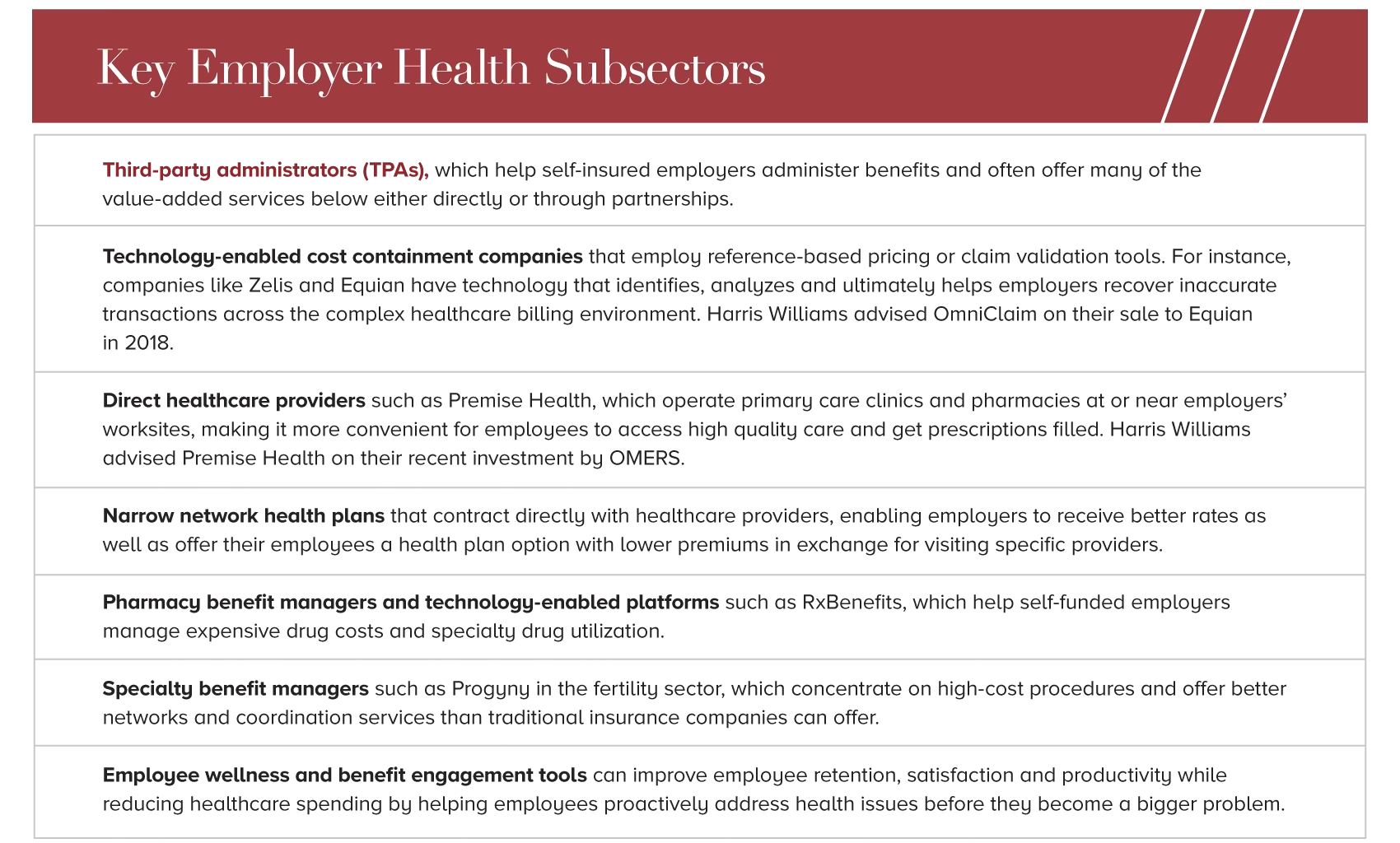

This article concentrates on third-party administrators (TPAs), which help self-insured companies manage their health insurance plans.

Increasing Strategic Value from TPAs

In just the past few years, healthcare costs have ballooned at a rate far beyond the country’s economic growth. Between 2012 and 2020, healthcare costs grew 50%.1 As the population ages and chronic conditions become more prevalent, these costs will only continue to grow.

With these expenses skyrocketing, company CEOs have zeroed in on novel mitigation strategies. For many, such cost reduction involves self-insuring: taking on the financial risk of paying for healthcare versus paying an insurer to assume that risk. For those who choose to self-insure, third-party administrators (TPAs)—companies that employers can engage to help manage company health insurance plans directly or through partnerships—are now an attractive option. And that’s creating strong interest among M&A investors looking for new growth opportunities.

“Historically, TPAs were seen as administrative and claims processing solutions,” says Nick Owens, a director in the Harris Williams Healthcare and Life Sciences Group. “That’s changing, with self-insured employers increasingly relying on their TPA partners to help implement cost mitigation strategies and drive engagement.”

Owens notes that insurance company Administration Services Only (“ASO”) offerings often do not offer the plan flexibility and ability to integrate best-in-class cost containment tools in the same way that an independent TPA can. “Successful TPAs help their clients think through plan design, reference-based pricing tools, and dual-option plan strategies,” he says. “This evolution has led to increasing strategic importance of the TPA relationship, and is driving longer-term, stickier relationships for both commercial and specialty-sector TPAs.”

The Growth of Self-Insurance

Consider the following:

Two decades ago, 60% of U.S. companies with 200 or more employees chose to self-insure their health benefits. By 2017, that figure had grown to 80%.2

Today, nearly 160 million Americans are insured by an employer offering a self-insured plan.3

Nine out of 10 workers at enterprises with at least 5,000 employees are now covered by self-funded plans.4

Approximately 8,000 employers in the U.S. that employ more than 1,000 people are self-insured (excluding quasi-governmental entities, such as universities and school systems, and labor unions).5

North Carolina leads the country in self-insurance, with 53% of employers offering a self-insured plan; four other states (South Carolina, Ohio, Wyoming, and Indiana) have at least 50%, and 20 more states have at least 40% self-insured.6

According to Derek Lewis, a managing director in the Business Services Group, the growing popularity of self-insurance is easy to understand. “It`s largely due to the fact that employers that self-insure typically pay less than they would for coverage underwritten by traditional insurance companies,” he explains.

Lewis adds that self-insurance is also becoming more accessible due to the growth of captive insurance arrangements. These are similar to self-insurance, but allow small employers to cluster together to gain similar levels of control and cost savings as those provided by traditional self-insurance. “Captive solutions are making it easier for smaller employers to reap the benefits of self-insuring, which, in turn, has increased the addressable market and revenue growth rates for TPAs,” says Lewis.

However, while self-insuring can reduce costs, it can also drive effort levels higher for employees. “Self-insurance requires significant administrative work, which can be time-consuming, expensive and difficult for employers to manage themselves,” says Cheairs Porter, a managing director in the Healthcare and Life Sciences Group. “That`s what drives growing demand for TPAs.”

The TPA market has grown steadily—by 6% since 2010—and is now an $8 billion sector.7 TPAs have been able to grow as more companies self-insure, filling a need while maintaining trusted, direct employer relationships with their clients.

Four Qualities of Standout TPAs

Drawing on its industry expertise, the Harris Williams team has identified four qualities that make certain TPAs particularly attractive to potential acquirers: client mix and specialization, value-added capabilities, the effective use of technology to provide seamless customer and consumer experiences, and proprietary provider networks.

1. Client mix matters.

Specialty subsectors such as Taft-Hartley funds (also known as multi-employer plans) and the public sector have higher barriers to entry because of the need for deep industry knowledge and expertise. Owens says these subsectors also can offer more low-hanging fruit from a cost reduction standpoint for employer clients. For one thing, they are less likely to have already outsourced plan management than other subsectors. In addition, Taft-Hartley funds are complex entities managed by boards of trustees staffed with similar numbers of union and employer representatives. The plans are challenging to administer due to the specialized capabilities required to handle contribution accounting and fund accounting and guarantee satisfaction among union members.

Owens adds that more complex clients such as Taft-Hartley funds are generally not well-served by insurance company Administration Services Only (“ASO”) offerings. “TPAs have been able to take share from larger ASOs by administering more flexible and customized benefit plans and higher service levels,” he says. “Offering innovative solutions, flexible plan design, and high service levels for middle-market clients has been a winning formula.”

2. Value-added capabilities increase a TPA`s value proposition and present an opportunity to offer complementary tools that drive down employer costs.

These integrated solutions often have a technology angle and can be internally developed or facilitated through a third-party partnership. Such capabilities enable TPAs to offer more bespoke and comprehensive solutions and build alternative business models that are data-centric and mutually beneficial.

For example, some of the more successful TPAs have replaced the typical PPO-billed charges with reference-based pricing capabilities that are either internally developed or outsourced to a partner vendor. This can result in significant savings for self-funded employees. Another example is care management strategies that use data to identify high-risk members and deploy clinicians to coordinate care and help those members make better healthcare decisions, increasing member satisfaction and reducing costs.

3. The ability to provide a seamless end-user experience differentiates a TPA in today`s complex healthcare market.

TPAs are increasingly cognizant of not just the customer experience, but also that of the end-user, the employee. As the breadth and depth of benefit plans and options expand, the employee experience is becoming a critical linchpin in the TPA`s service offering—especially functionality that helps employees manage payments and track spending in different accounts.

“Companies want employees to use their benefits, and to select those benefits that best meet their individual needs,” says Sam Hendler, a managing director in the Technology Group. “TPAs are investing in technology to provide a better user experience for both the employer and the employee. Platforms that help express the different options available to the employee and, most importantly, help end-users make better decisions are extremely valuable.”

Dan Linsalata, a director in the Technology Group, concurs. “As you get into larger organizations, or multi-employer health plans, there are very complex and compliance-intensive processes and workflows. The more technology-enabled automation you can put into that, the better the experience for the end employee. Operations run more smoothly and efficiently for the employer as well.”

For example, ConnectYourCare (CYC) offers a SaaS platform for consumer-directed healthcare and benefits account administration savings, payments, and claims substantiation. “Platforms such as CYC`s provide a great self-service experience for the employee, and greater efficiency for the employer`s HR team because they receive fewer questions,” says Hendler.

4. Owning a proprietary provider network can help differentiate a TPA.

TPAs that have their own proprietary provider networks deliver higher profit margins and are better positioned to compete with insurance company ASO offerings. Network ownership also facilitates the development of narrow network health plans, which are plans contracted directly with health providers. These plans provide lower rates to employers, allowing them to offer health plans with lower premiums to employees in exchange for visiting specific providers. Proprietary provider networks and narrow-network health plans can drive even greater cost savings for self-insured employers while reducing premiums for employees.

Conclusion

As healthcare costs continue to rise, employers are taking control of the situation by self-insuring and partnering with technology and service providers to better manage costs. TPAs make benefit administration less burdensome for companies that choose to self-insure, allowing employers to focus on their core strengths and functions. TPAs have proven to be valuable assets to self-insurance programs by mitigating costs without sacrificing quality healthcare for employees.

Recent M&A activity and steadily climbing multiples indicate that TPAs are gaining the attention of investors. Major health insurers United, Anthem, and Centene have also made significant TPA acquisitions in recent years, proving strong interest from financial and strategic investors alike. Because of the significant value they create, we believe TPAs will be on the radar of M&A investors for years to come.

Select Relevant Harris Williams Transactions

The Harris Williams Healthcare & Life Sciences (HCLS) Grouphas experience across a broad range of sectors, including healthcare providers, payors and payor services; outsourced pharmaceutical services; medical device supply chain; healthcare IT; and pharmacy. For more information on the HCLS Group and other recent transactions, visit the HCLS Group`s section of the Harris Williams website.

The Harris Williams Business Services Grouphas experience advising companies that provide a range of commercial, industrial and professional services. For more information on the firm`s Business Services Group and other recent transactions, visit the Business Services Group`s section of the Harris Williams website.

The Harris Williams Technology Grouphas deep domain expertise in software and technology-enabled services and dedicated focus areas across a variety of vertical software applications and end-markets. For more information on the firm`s Technology Group and recent transactions, visit the Technology Group`s section of the Harris Williams website.

Published August 2021

2. “American employers are in the healthcare business,” Collective Health, February 28, 2018, https://blog.collectivehealth.com/employer-driven-healthcare-270bfb7ee8c7

3. Merritt Hawkins, CMS, CDC, and Partnership to Fight Chronic Disease

4. “American employers are in the healthcare business,” Collective Health, February 28, 2018, https://blog.collectivehealth.com/employer-driven-healthcare-270bfb7ee8c7

5. “Employer Trends in Self-Insured Health Plan Coverage,” Employee Benefit Research Institute, September 5, 2019, https://www.ebri.org/docs/default-source/infographics/36_ig-selfinsur-5s...

6. ibid

7. “Self-Insured Health Benefit Plans 2020 Based on Filings through Statistical Year 2017,” Advanced Analytical Consulting Group and Deloitte, February 20, 2020

Select Activity

Contacts

Nick Owens

Managing Director

Dan Linsalata

Managing Director

Cheairs Porter

Group Head

Managing Director

Derek Lewis

Group Head

Managing Director